Q1. When does the new tax laws take effect?

- Application of the Nigeria Tax Act will take effect on 1 January 2026.

The four Acts are:

Nigeria Tax Act 2025 (NTA 2025)

Nigeria Tax Administration Act 2025

Nigeria Revenue Service (Establishment) Act, 2025

Joint Revenue Board of Nigeria (Establishment) Act, 2025

Q2. Will deposits or transfers into my bank account be taxed?

- No, mere deposits or transfers into your bank account are not automatically taxed. However, deposit or transfer that constitutes an income into your bank account may be reviewed for tax purposes where your income exceeds the exemption threshold for small business and companies. So, it will be good to have a clear narration on all banking transactions.

Q3. Will tax authorities now monitor my bank accounts in order to charge tax?

- Tax Authorities are applying digital tools more than ever before , Section 29 (1-3) NTAA requires banks and financial institutions to render returns to the revenue authorities where monthly cumulative transactions exceed N50million and N250 million for individuals and businesses respectively..

- The Act also empower Tax Authorities to request certain information from Financial Institutions

Q4. Does the tax authority have the power to debit my account without any form of engagement/notice?

- No, the tax authority does not have the power to debit your bank account without any form of engagement. The law only prescribes a power of substitution which suggests that the tax authority can appoint any person to assist with the recovery of taxes due, where the tax payer has failed to pay after series of demand notice/letter has been served. [Section 60-63, NTAA]

Q5.Will my bank account be closed on 1 January 2026 if I do not have a tax a taxpayer ID?

- No, the law does not mandate banks to close your accounts where you do not have a tax ID. However, the law requires a person engaged in banking, insurance, stock-broking or other financial services in Nigeria to ensure that every taxable person provides a Tax ID.

- This is not a new requirement of the law. [Section 8, NTAA] In addition, the Nigerian Tax ID Portal has been linked to the National Identification Number (NIN) data base for ease of generating and retrieving tax ID in Nigeria.

- Individuals and Corporate Bodies can get the Tax ID using this Link https://taxid.nrs.gov.ng/

- It is strongly advised that all Bank Customer update their records. Note provision of Tax ID does mean tax will be applied on your account.

Q6. As a Nigerian that relocated abroad, will the remittances in my bank account be taxed.

- No, remittances into your Nigerian bank account will not be liable to tax as this income has already suffered tax in the source country. In addition, it does not constitute an income arising from a new economic activity.

- [Section 17, NTA clearly state that incomes earn by Non Resident in Nigeria are Taxable in Nigeria. In effect NRI who earn income in Nigeria are expected to pay Tax on Income earn in Nigeria.

Sec 150 (1) of NTA States. A non-resident person who makes taxable supplies to Nigeria shall register for tax and include VAT on its invoice for all taxable supplies.

Sec 150 (2) Where a non-resident person is making taxable supplies from outside

Nigeria to persons in Nigeria, the taxable person to whom the supply is made

in Nigeria shall withhold the VAT due on the supply and remit it to the Service.

Q7. As a Nigerian that relocated abroad, will the remittances repatriated to my family in Nigeria be taxed in their bank accounts?

- No, gift is not taxable inflow as they do not constitute a transaction resulting from an economic activity. [Section 4, 163 ΝΤΑ].

Q8. As a Nigerian that relocated abroad, does having a permanent place for my domestic use in Nigeria mean I will pay taxes on the income earned from my new country of residence in Nigeria?

- No, taxes will still be paid to the country you earned your income. However, you may use the taxes paid in the source country as a credit to offset taxes due in Nigeria based on unilateral/bilateral tax rules. See item 6 above

Q9. As a remote worker in Nigeria, am I liable to pay tax on income earned from abroad?

A:Yes, income gains or profits of an individual who is a resident of Nigeria are deemed to accrue in Nigeria and are chargeable to tax in Nigeria wherever they arise, and whether or not the income, profits or gains have been brought into or received in Nigeria. However, please note that tax will not be deducted at source from your bank account.[ Section 12, NTA]

Q10. Is it true that individuals earning below National Minimum Wage or N800,000 per year are exempt from tax?

- Yes, individuals earning up to National Minimum Wage or

N800,000 per year are exempt from PIT, reducing the burden on low-income earners. Based on PAYE computation an individual earning less thanN1,200,000 will not be taxed.

Q11. Are scholarships, grants, or awards considered taxable income?

- Scholarships to students are not taxable. However, grants and awards are considered taxable income where they are not specifically exempted. [Section 4, NTA]

Q12. As an individual or an unincorporated business owner, will I pay personal income tax or company income tax?

- If you run a sole proprietorship or unincorporated business (just you, or you and partners, without forming a limited liability company), then you pay Personal Income Tax (PIT) on your business profits (plus any other income).

- Small Company provision of N100m turnover and N250m Assets is also only applicable to Limited Liability Companies, unincorporated businesses who are doing less than N100m are advised to upgrade to a Limited Liability Companies.

Q13. Are salaries of military officers taxable?

- NTA exempts wages and salaries of military, Police officers from tax. [Section 162, ΝΤΑ]

(o) emoluments of any person serving as other rank and other personnel serving in combat zones, hazardous areas or in designated operations, provided that where any other income accrues to the person, not being income by way of personal emoluments, that income shall be liable to tax under Chapter Two of this Act ;

Q14. As a pensioner, will my pension be taxed in 2026?

- Pension funds and assets, gratuity or any other retirement benefits are exempted from taxes. [Section 162, NTA]

- However, any other no pension income is subject to Nigerian Tax.

Q15. Under Capital Gains Tax – If I sell shares and make a profit, will I be liable to tax in 2026?

- No. Except where disposal proceeds, in aggregate, is more than #150 million, the chargeable gain exceeds #10 million in any 12 consecutive months and where the proceeds are not reinvested. [Section 34, NΤΑ]

Q16. Are cooperative societies or informal enterprises included in the new rules?

- Registered cooperative societies remain tax-exempt as long as they do not engage in profit-making business. See extraction below:

(ii) a co-operative society registered under any enactment or law relating to co-operative societies, not being profits or gains from any trade or business carried on by that society.

From above exemption granted to cooperative societies and other exempted entities are limited to activities relating to cooperative societies, other activities like placement of funds remain Taxable.

Q17. I own a company engaged in agricultural business; will it be liable to tax in Nigeria?

- Companies engaged in “agricultural businesses” e.g. crop production, livestock, aquaculture, forestry, and dairy get a five-year tax holiday from Company Income Tax (CIT), starting from when the business commences. [Section 162-P of NTA]

Q18. Definition of Small Companies: How much must a company earn to become liable to pay taxes?

- CIT rate remains 30% for other companies and 0% for small companies. “small company” means a company that earns gross turnover of

N100M or less per annum with total fixed assets not exceedingN250 million. Any business providing professional services shall not be classified as a small company. - Unincorporated establishments (Enterprises, Ventures, Partnerships. Etc) are not covered under this exemption, their Profits will be taxed using Pay As you Earn Tax Band.

Q19. Do I have to write Tax ID on my Invoices

- Section 100 of NTA Imposes an administrative Penalty of N5m on a Statutory Body of Company who award contracts to an unregistered person. We advise companies to fully comply as administrative Penalty is an open ended one, the Law did not state clearly how it will be applies, is it per transaction, or per Vendor,..

- The Section also stipulates Penalty for individuals who refuse to Register ( See below)

Q20. STAMP DUTY

- Stamp Duty on Electronic Transfers- The new law changed the name of Electronic Money transfer to Stamp Duty, the amount which remains N50, will now be borne by the Transferor

- Stamp Duty on Loan restricted to Loan ten ored above 12months and the rates depending on the collateral security are now clearly stated. Meanwhile, loan within 12 Month will be charged to fixed rate of N1000 or N500 depending on Security types.

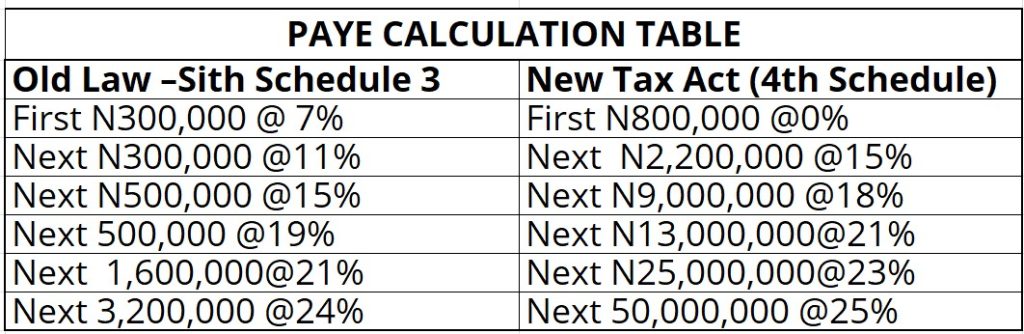

Q21. How is PAYE Calculated

- Paye is calculated using the below band after exemption:

- Rent allowance 20% of Annual Rent subject to N500,000

- National Housing Fund Contribution

- Interest Paid on Owner Occupier Residents

- Employee Pension Contributions

- Also note: that individuals will need to file for Tax aside from employer filling done by their organization

Q22. How Company income Tax (CIT) Calculated

- CIT rate remains 30% , Plus 4% for Development Levy

59.—(1) A development levy of 4% is imposed on the assessable profits

of all companies chargeable to tax under Chapters Two and Three of this Act,

other than small companies and non-resident companies.

- Effective tax rate is now 15% where computed ETR is lower than 15% , the company will pay top up Tax In compliance with OECD.

The OECD (Organisation for Economic Co-operation and Development) is an international organization that works to shape better policies for better lives.

Please note that above should not be construed as Tax Advisory, individuals and Companies are advised to read the law for proper understanding and also contact professionals where necessary.

This article is issued to the best of our knowledge based on the Nigeria Tax Act. Jtax Consulting and its Partners will not be responsible for any liability resulting from placing reliance on it.

Contact us – 08129201934